This is the most comprehensive guide to getting unbiased financial planning service in Malaysia.

We are going to show you everything you need to know when it comes to engaging a qualified and credible financial planner.

I think you agree that it is not easy to find a credible financial planner in Malaysia.

On the other hand, it is too easy to encounter a bad one (pushy financial sales agents masquerading as ‘financial planner’ or financial adviser or financial consultant).

We’ve heard and seen cases whereby the blatant misconduct by certain financial agents in the financial planning industry gives financial planning profession a bad name.

Times are changing, however, because a select few financial planners in Malaysia have evolved to being certified and fee-based financial planners.

This guide explains how to identify and hire a good financial planner in Malaysia, which will really benefit you, your family and even your career or business.

At the same time, it will help you to maximize the benefits of engaging a financial planner with the fees you pay.

Table of Contents

A) 10 Factors to consider before engaging a financial planner in Malaysia

1. Set and communicate expectations to a financial planner so they are met

Taking time to determine what are the financial goals you want to achieve is the first step towards deciding how effectively you will be working with a financial planner in Malaysia. It is also important to consider which area of financial planning you need assistance on. Same like when you see a doctor, if you don’t tell the doctor which area of your body you feel ill, even the best doctor would not be able to treat you.

2. Evaluate your own Competency of financial management and financial matters

If your knowledge of personal finance is limited, the expertise of a licensed and certified financial planner in Malaysia context would be crucial. Why? Because he must be competent to draft your financial plans and advise you holistically in complex aspects of personal financial management in realizing your financial goals. Check the qualifications and license of the financial planner, to ensure his/her qualification is recognized and his/her practicing license is valid.

Note: A financial planner need to undergo certification, then only he or she gets licensed, not the other way round.

3. Determine Level of involvement in financial planning process

Decide in the beginning whether you would rather carry out your own investment plan, also know as be your own investment analyst (hence seeking only second opinion advice from the financial planner) or rather have the financial planner assists you in executing the plans.

4. Gauge Complexity of financial situation

This will directly impact the degree of involvement of the financial planner. For example, the needs of a single young adult differs from a middle aged family man. This is also knowing as scoping the aspects of financial planning services you need advice on.

5. Forming Relationship with the financial planner

The frequency of contact that you desire with a financial planner should also be considered, which is why it would be tricky if your financial planner is based in other cities in Malaysia although the use of technology like video conferencing can bridge that. Also, whether you want to review the financial plan half yearly or annually or more frequently is also a factor to consider in hiring a financial planner in Malaysia.

6. Consider the cost of hiring a financial planner

The amount of which you are willing to pay a financial planner in question would also be an important deciding factor in how to engage the services of a financial planner. You are advised to discuss the compensation structure with the planner at the onset. Having a clear understanding of how the financial planner is being compensated for the financial planning work done would prevent any misunderstanding later on.

7. Familiarize yourself with financial planning terminologies and concepts

It would be in your best interest to be prepared and to learn about financial planning concepts and the language often used by financial planners. While you may not be familiar with all financial planning terminologies used in the beginning, it would be good to know at least the basic terms used.

8. Obtain referrals and interview more than one financial planner

Just as you shop around before purchasing an item, it would be wise to speak to family, relatives, colleague or friends so that you may get referrals from the parties you trust. Or Google it! By searching for financial planner near you or residing in your city. It is also better to speak to more than one financial planner until you are able to select one whom you trust with your financial information with.

9. Check the financial planner background and obtain references

Since the financial planner would be privy to one’s financial information, it is advisable to verify the financial planner’s background by checking with their professional associations or any regulatory bodies. A licensed financial planner whom is in the full time, long term financial planning practice would not be folly to shoot himself in the foot by leaking client’s financial information to any third party without client’s consent as it would soon mean end of business for him.

10. Document of scope of services in black & white

Remember to request any advisory contracts or engagement letters in writing to document the nature and scope of work to be provided by the financial planner. This is also to avoid any misunderstanding later on.

B) 7 benefits can a financial planner in Malaysia bring you

A true financial planner should be fee based, whereby he charges a professional fees just like your doctor, lawyer or accountant. [Also read: Why financial planner charges fees]

But,

Do you need a financial planner?

Is a financial planner worth it?

To answer that question, first of all, you want to understand if below is something you can do on your own.

Financial planning, in its truest sense, is not about products. Financial planning process consists of 6 steps. What are the six steps in the financial planning process? I show you below.

In summary, they are:

- Setting and establishing expectation and key deliverables from a financial planner

- Fact finding to set a baseline, including understanding your financial goals.

- Analyze, dissect and evaluate all financial information and their correlation

- Develop actionable financial plan, recommend next steps to take by considering all feasible alternatives.

- Implement the financial action plan, and.

- Monitor, reevaluate and revise the financial plan periodically

Depending on the scope of advisory provided by a financial planner, the outcome of a comprehensive comes in the form of a financial plan development. A full-fledged financial planning process enables you to make better financial decisions because it…

- Integrates every aspects of your personal finances and shows you how one aspect correlates with each other.

- Contains a snapshot of your financial health, just like a blood test

- Analyzes your unique financial situations in increasing the odds of achieving your financial goals

- Identifies blind spots in personal financial management you may have overlooked

- Optimizes your money management

- Gives custom-tailored made recommendations to achieve these financial goals

- Gives you better peace of mind

Also read: Financial Planner CFP Penang

A true financial planner acts as your fiduciary advisor, who can make you feel more secure and confident (sometimes making you see the light at the end of the tunnel) in achieving the many often conflicting financial goals with the resources you have.

For many people, that is commonly known as achieving Financial Independence and Early Retirement. As someone who had experienced it, let me explain to you what Financial Freedom really is and what it is NOT.

Financial planning, from a technical standpoint, boils down to this – “Solving life’s mathematical equations.”

Don’t you agree life is a collection of ever changing and often conflicting financial goals?

If life were so simple as just having one financial goal (for example, retirement planning), this mathematical problem is as simple as 1 plus 1 equals 2.

Simple and straightforward.

Everyone can do some extrapolations, and working backwards some figures using a simple retirement calculator – walla!

You would have a personal financial plan or a financial roadmap laid out in front of you. No need for any financial planner.

But the complexities come when we desire more things in life. It is not wrong, in fact it is normal.

- We want the best for our children education – which is really, the major dent to any parents’ finances.

- We also want to go for that dream vacation, purchase our dream house, etc.

- And at times, life throws us a curve ball that not only “dents” us emotionally but financially as well – like, chronic illnesses.

Now, the roadmap to our ultimate goal – comfortable retirement, doesn’t appear as straightforward as we have thought, aye?

To complicate matters, there are external factors beyond our control that also comes into our life equation – the likes of

- inflation,

- fiscal policy,

- monetary policy,

- bull cycle,

- bear cycle

What about retrenchment? It is pretty common nowadays, yes?

With all these variables, how is our roadmap going to look like? From a simple 1+1=2, this has ballooned up to a complex calculus equation.

Can you solve this on your own?

Or would you want to solve this at all or just let things run its own course?

More often than not, unlike a true mathematical problem, there is NO right or wrong answers when solving life equations.

It depends on which area you are willing to adjust and compromise. For example, delaying retirement age or lowering post retirement lifestyle expenses.

Don’t you agree money is a sensitive subject?

We deal with it everyday in our adult life but we tend to avoids talking about the bad sides of it.

In the end, money is just money, but in actuality, our emotions are at stake. We are depressed when we have less money, and are in the highs when we have more money.

To reduce this emotional volatility, the same way we wants to reduce volatility in our investments, is to have a financial roadmap described above.

Let me give you an analogy if today, you have an abdomen pain, you and your family will worry day and night, right?

Your emotions will be affected.

So what you do?

You would be willing to fork out money to do medical checkup.

Now, the outcome of this might be good or bad.

Good is the doctor might tell you – it’s just indigestion problem and will go away in a week’s time.

Bad is you have cancer.

Either way, you know what to do from now on instead of guessing.

As a result, some of the common questions can be answered with clarity by engaging a CFP financial planner to solve life’s mathematical equations like a financial analyst:

- Am I on track and making the right financial decisions toward my retirement?

- Can I afford my children education without jeopardizing my own retirement nest egg?

- Am I optimizing my investment returns? Can I do better? How?

- Is there a way to have more surplus without cutting down?

- What is my current financial health condition?

- Am I overpaying for my insurance premiums?

- How can I get sufficient human life value protection for my family and business?

- How can I visualize the cause and effect of my multiple financial goals?

- What are the best financial products in the market & who can do an objective comparisons?

- What should I do with my business so I can retire while still reaping passive income from it?

- How do I preserve my wealth for my family after I pass on?

- How can I avoid making costly mistakes that will jeopardize my retirement?

Moving on to the next level, financial planning will also helps you achieve an optimum fulfillment in life.

We also call this – Financial Life Planning, achieving maximum happiness with the optimum money spent – whereby return-on-life (RoL) is more important than return-on investment (RoI).

The 3 crucial questions to ask in our financial life planning are:

- How can I derive the most meaning from my means (money)?

- Is the fulfillment received in proportion to the money spent?

- Is this in alignment with my values, goals and purposes?

Financial life planning revolves around developing the skills and mindset to:

- Achieve enough means to align with our life meaning

- Recognize when we have achieved enough

- Stay near the peak of life fulfillment without falling back into deprivation or gluttony

This must be further explained using the Fulfillment Curve.

Using a Home Buying analogy to further explain this:

1 – You are essentially homeless; you sleep under the bridge.

2 – You own an extremely cheap, extremely small old flat. That means there’s barely enough room of sleeping space for all family members or room to do anything at all. You are embarrassed to have guests at all.

3 – You own and stay in a nice condominium with facilities. There’s enough room for everyone but you are sometimes pinched for space and there’s more clutter than you’d like. You sometimes have your friends over, but still, you feel pretty self-conscious about the place and don’t have the dinner parties you’d like

4 – You own a semi-detached house which is just the right size for your family. You feel comfortable having any and all guests over, the housework doesn’t overwhelm you, and the bills are completely affordable.

5 – Your house slightly exceeds what your family needs, but it gives you ample of room to grow. The bills are slightly painful, but you can still manage it. You spend a bit more of your weekends on home cleaning and maintenance than you’d like, but you feel quite proud giving dinner parties and inviting people over.

6 – Your house is a freaking mansion. We can afford the bills, but just barely, and only if you don’t eat out often. The bills make you feel kind of guilty, and there are times where it feels like all you do is earning your income just to pay for the bills.

7 – You over leveraged bought a house ten times your annual income to impress your friends and relatives. Your house is mind-blowingly awesome, but just last week, you just got retrenched from your job.

Point#1 – The fulfillment curve applies to everything where money is spent on.

The basic principle applies to almost everything in our life, from food to clothing to shelter up to hobby-oriented activities. In almost every aspect of life, the point of maximum enjoyment is not the point of maximum spending – spending too much reduces fulfillment.

Point#2 – Guilt is one of the surest signs of the downside of the curve.

If one feels guilt about spending in any area, he is likely spending more than his natural fulfillment peak. Take a few steps back on that spending some and you’ll almost always find that things to return being enjoyable again.

Point#3 – Your fulfillment curve peak might actually come with spending no money at all.

Here’s an example: family time spent with your spouse and/or kids playing at a neighborhood park on a Sunday morning. The cost is virtually nil, but it was a peak on the fulfillment curve. Fulfillment curve peaks don’t ncessarily have to cost you.

Point#4 – Fulfillment curve vanishes by Routine frivolous purchases

Like a RM 15 Starbucks coffee each morning – are beyond the peak, whether you actively notice it or not. If you do it every day, it’s no longer a treat. It’s not something special to really bring you fulfillment. Try drinking cheap coffee at the office all but one day a week. You’ll find that the one good coffee you do drink brings you far more fulfillment than it used to.

C) 4 Reasons to engage a financial planner in Malaysia instead of DIY financial planning

DIY financial planning essentially refers to one taking on a task in an area without engaging the direct aid of experts or professionals.

In this age and time where almost every answer to a problem or question can be found on Google or YouTube, what can’t we do ourselves?

It is commendable that a growing number of Malaysians actually recognize and acknowledge the need to address financial planning at this point in their lives. They see themselves as well informed and primed to take the next step in planning for their financial future as the advancement in financial technology coupled with an increasingly tech savvy population has resulted in people empowerment.

Countless websites are offering free financial calculators, price and product comparison tools.

Even virtual fund managers (a.k.a. robo-advisors) are now a trend. Supported by the emergence of a plethora of personal financial products available online, it would seem that creating one’s own financial plan is just a mouse click away without any involvement from a real life person.

With so many financial tools at one’s disposal, it is easy for one to take on the role of becoming one’s own financial planner.

But is it really that simple? Can DIY be the solution or does it simply present itself as an illusion of one?

The ILLUSION

The underlying reasons why many individuals are inclined to go down the path of DIY financial planning are deep rooted in their preconception towards how financial planning should be done, such as:

- I am in the best position to know my own finances and investment style;

- Privacy is important to me. I am not comfortable disclosing every single detail of my finances to an outsider;

- By doing it myself, I retain better control over where my money goes;

- I do not want to take unnecessary risks by outsourcing to a 3rd party;

- I am a highly qualified professional myself (e.g. accountant, financial controller, banker) and thus am more than capable of doing my own financial planning; or

- I have very simple, safe, straightforward strategies and lifestyle (i.e. money in fixed deposits, no debts or dependents) so I can manage myself.

Proponents of DIY financial planning would also argue that going direct into the online financial products marketplace by far and large confers the benefits of time saved, money saved and you get to have your own say with what to do with your hard earned money.

What the individual fails to realise when he steps into the shoes of becoming his own financial planner is that there exists a void between the financial planning tools he is using and the products that he subsequently buys.

Not only are the tools and products completely independent and detached from each other, there is the total absence of follow through from the planning to the execution stage.

Let me Tell you the Analogy using a Financial Planning Elephant

This story is an old Indian folk-tale about 6 blind men and the elephant.

Each blind man is asked to walk up to the elephant, experience the elephant, and then describe what an elephant is.

- The first blind man walks up, wraps his arms around the back leg, and says, “An elephant is like a large tree trunk.”

- The second blind man walks up, holds the tail in his hands, and proclaims that “An elephant is like a thick rope.”

- The third blind man walks up, holds the ear, lets it fall back to place, and says, “An elephant is like a giant fan.”

- The fourth blind man walks up, touches the tusk, feels the tip of it, and says, “An elephant is like a huge spear.”

- The fifth blind man walks up, touches the side of its body, and exclaims, “An elephant is like a brick wall.”

- The sixth blind man walks up, holds the trunk in his hands, and proclaims that “An elephant is like a python.”

Each blind man is accurately describing his experience of the elephant, but none of them understands all of the parts or how they fit together.

This is the exact same problem you face when learning to do DIY financial planning!

The teachers are blind men telling half-truths based on their limited understanding of how the financial freedom elephant is put together.

Unfortunately, when you try to build your wealth based on half-truths the result is usually failure (as the statistics prove).

What you need is a foreman with the experience and know-how to put all of the pieces of the elephant together.

Each Of These Principles Is A Separate Piece Of The Financial Freedom Elephant Puzzle

(Like The Leg, Tail, Or Ear – Dangerous Half-Truths),

But It Is Only When They Are Connected That You Experience The Entire Elephant.

- Frugality gurus teach you to spend less.

- Entrepreneur and career gurus teach you how to make more.

- Investment gurus are all about investing wisely.

- Productivity and professional development gurus show you how to take consistent and persistent action.

- Almost no gurus teach you how to design a wealth plan based on proven principles. (Guess they missed that piece of the puzzle entirely)

Notice how the other gurus blindly portray financial freedom as if it only requires the one limited, separate, half-truth piece of the elephant they understand.

In the context of financial freedom, they are all blind men teaching half-truths.

The financial freedom elephant is a complex puzzle where all these half-truths must be connected into a congruent whole if you want to actually achieve the goal.

While the majority of people fumble and fall short with fragmented half-truths, the select few who figure out how to connect the puzzle pieces are the ones who reach their goal of financial freedom.

The role of a financial planner can be summarized using 3 analogies below:

The Architect

Imagine undertaking a 10 years mega home construction project . Think of having to manage civil engineers, electrical engineers, mechanical engineers, contractors, interior designers, etc on top of your full-time job or business. You need to ensure everything and everyone is coordinated – so that the end result is what you envisioned.

TEDIOUS? We thought so too.

Now, imagine the pivotal role of an architect who fully understands what you need, and manage your home construction project.

A financial planner is the Architect of your Personal Finances – making sure it meets your desired outcome. And your Personal Finance is, in fact, a Dynamic Long Term Mega Project.

The Doctor

Imagine you wake up one day and feel prolonged uneasiness in your chest. Do you prescribe your own medication? Or…does it feel right if a medical professional dispenses medication without proper consultation and diagnosis?

NOPE? We thought so too.

Getting the wrong or unnecessary medicine not only worsens your condition, but can possibly endanger your life.

Doctors charge for diagnosis (consultation), and only dispense suitable medicine (solutions) as required. They are billed separately. It should be that way for your best interest as a patient.

It works the same way for a true fee based financial planner.

The Mechanic

Imagine a highly-educated you, driving a nice continental car. Do you fix your own car when discover a potential problem – like, a loud rattling sound under the hood?

NOPE.

You bring your car to your trusted mechanic at a reputable service center, because he is highly skilled and trained in this area – although he may not have a diploma/degree.

Can you be your own DIY mechanic? Of course you can – everyone can learn being one, given the time and training.

But you’ll find out that it’s not worth the trouble, and you can afford to pay the mechanic to get your car fixed in no time. You are smart to leverage on the mechanic’s practical experience.

Even as you engage a fee based financial planner in Malaysia, you are still the ultimate decision maker.

You are completely involved in the entire financial planning process from start to end.

You are in control.

This is because the real concept of working with fee based financial planner does not mean outsourcing your financial planning but rather, working hand in hand with your financial planner in a symbiotic partnership.

Your financial planner is able to complement what you do in order to help you achieve your desired financial freedom by maximising your strengths while minimising your weaknesses.

Any potential problems can be resolved quickly and effectively, leaving you with more time to do things that matter more.

In conclusion, DIY financial planning may be able to address certain aspects depending on the individual’s experience and expertise. However, you may find that you might excel in a few areas but would have gaps in others.

In that sense, optimizing your money then becomes a behemoth task when each area of your personal finance is not managed as one cohesive function.

In fact, the DIY financial plan may even create a false sense of comfort, security and sufficiency, preventing one from reviewing his financial needs and requirements that may change from time to time.

As such, instead of doing it yourself, it might be worth your effort to sit down and have a chat with your financial planner. Putting ego aside – do it together instead. A little time spent now would save you more time (and pain) in the end.

“You engage a financial planner not because you’re not smart enough to do this yourself.

But you hire one because he is not you.”

D) The 9 criterion to look for in a financial planner

A reputable fee based, true financial planner should possess the following qualities:

1) Be licensed by the Securities Commission

In fact, all practicing fee based financial planner in Malaysia are required to be licensed by the Securities Commission.

Ensure that your financial planner is licensed and adhere to financial planning practice standards. Also check with the professional body in which he is affiliated with or check the Securities Commission website at www.sc.com.my

2) Possess qualifications recognized by regulatory bodies

It is vital to ensure that your financial planner is well qualified.They are certified or qualified by professional bodies like CFP Board and/or Financial Planning Association of Malaysia (FPAM) or Malaysia Financial Planning Council.

A good example of the relevant professional designation is the Certified Financial Planner (CFP CERT TM) certification.

Certified Financial Planner CFP is the basic education requirements and financial planning certification.

You can also check out the list of approved financial advisers at Bank Negara Malaysia website.

3) Have adequate experience

A good financial planner is one who has the expertise to help you meet your financial goals – be in short term or long term.

However, one should also take into account whether the financial planner is close to retirement or if he is going to be available to assist you for an adequate period of time.

Also, if you are an expatriate, then it might be wise to engage an expat financial planner who has the experience dealing with financial matters in your home country.

4) Be trustworthy and open

A good financial planner is one whom you are comfortable with and who is honest with you. He should be someone who is forthright enough to tell you the facts as they are, yet understanding enough to ensure that you are comfortable dealing with them.

5) Disclose the compensation structure

Any financial planner should disclose all fees and compensation from the start. It is in your interest yo agree on the compensation structure before the commencement of the engagement. This is part of the important standards of professional conduct.

6) Be able to provide on-going service

You need a financial planner who can provide on-going service and is committed to develop a long term relationship with you.

It is of no help to you if the financial planner constructs a financial plan for you and then never contacts you again.

Constant contact is vital to ensure the success of the plan.

7) Assess your existing financial situations and identify your personal cum financial goals

A financial planner should review all of your financial records and help you to identify your goals before embarking on constructing a financial plan.

8) Explain the pros and cons of various options and products

It is the financial planner’s responsibility and professional standards to explain the different options available to you before recommending the best solution to meet your unique objectives.

9) Periodically evaluate your financial plan(s)

The financial planner should review your plan periodically to ensure it gets closer to your goals, and it isn’t, then actions need to be taken to bring it back to on-track instead of off-track.

E) 5 Aspects an independent planner is different from normal financial planner

Financial planning services in Malaysia is still in its infancy. More and more financial planners are recognizing that just selling financial products and receiving commission does not meet clients’ expectations.

To provide services which is of value, it is necessary to move to a place where financial planners become more consumer-centric and focus entirely on helping their clients achieve their financial goals.

They are a new class of people called independent, certified financial planners.

Info from insuranceinfo.com.my – Dealing with intermediaries

| Compare | Licensed Financial Planner | Tied Financial Agent | Examples |

|---|---|---|---|

| Minimum Qualifying Requirements | A Bachelor’s Degree, CFP certification (240hrs of lecture and 14hrs of exam) or RFP certification, 3 years minimum of relevant experience. | SPM, CPE (2hrs exam), CEILI (2hrs exam), CUTE (2hrs exam) | The Ivy league universities vs others |

| Approach and Methodology | Financial planning & systematic process or holistic approach, i.e. optimizing your current & future resources to your financial goals. In-house research on funds selection, life insurance plan stars rating and financial life planning / cash flow modelling. | Single need / piecemeal solution and pretty much product focused. | Chief Accountant / CFO vs Accounts executive. |

| No. of financial providers or solutions | At least two providers in life insurance, unit trust and PRS. In addition provide service like financial plan and estate planning, i.e. will writing, trust, biz succession planning, etc. | Cannot represent more than one supplier, and tied to its principal | 1-stop shop, e.g. Senheng Electric, senQ, Harvey Norman. |

| Interest represented / Client & Distributor (legal) Relationship | Client & Professional (i.e. FA) relationship. (Is required to purchase a Professional Indemnity insurance). | Client & Supplier (i.e. Insurer / Unit Trust Management Company) relationship (note: Agent acts as an employee of the supplier, and he/she has no legal relationship with the client) | External auditor vs internal auditor |

| Transparency of proposed solution | Impartial views (evaluating pros and cons of each possible solutions or products) and choices. | Biased view (pros only) and without choice | Senheng vs Sony/Apple Store |

| Continued education (CE) | SC (20hrs), BNM (20hrs), FiMM (16hrs), FPAM (20hrs) | LIAM (30hrs), FiMM (16hrs) | Doctors & accountants who needs to fulfill CE points to renew license |

For many years, the term ‘financial planners’ has been abused by tied financial agents who are masquerading as financial planners, where, in fact, they are only glorified sales intermediaries who do not take into account the holistic approach in planning your personal finances. You may came across the tied agents below who claim themselves as certified financial planners:

- Insurance agents

- Unit trust consultants

- Investment/wealth adviser or banker

- Real estate planner

In actuality, these are 5 non-negotiable MUSTs

- He holds the right regulatory licenses

- He charges a fee fro his advice and services

- The advice he gives is holistic in nature

- He has NO sales quota to meet

- He has access to a wide range of products

1. Financial planner who holds the right regulatory licenses

It is a simple approach because a licensed financial planner will disclose what licenses they hold as it certainly something that works to their advantage.

In fact, in Malaysia, any financial planner who claims to offer financial planning service must hold Capital Market Service Representative License for dealing in financial planning activities under Securities Commission.

This license allows the financial planner to charge fee for his financial planningwork.

Besides that, he also holds Financial Adviser Representative License under Bank Negara for providing risk management advisory work, relating to insurance products and recommend the appropriate solutions.

He can source insurance product from various insurance companies.

A practicing financial planner who wants to recommend and source unit trust from the various unit trust companies must hold the Corporate Unit Trust Advisor (CUTA) license under Securities Commission.

2. Financial planner who charges fee for his advice and services

Financial planning and advisory process should be free from commercial influence and vested interest of products provider that may result in an outcome that is suboptimal for you.

This is why fees first for advisory work before any products come into picture, just like doctor gives your consultation before dispensing medicine if required.

Having said that, there are 2 different approaches in fees:

- Fee-based: This means the financial planner charges a fee which reflects his time and billing rates to deliver holistic advisory services. He will derive extra income in the form of commission or in the form of asset-based management fee when he helps you to secure and implement the needed financial and investment products respectively.

- Fee-only: This means the financial planner does not receive any income from other sources such as provider of financial products. He will help you purchase the financial products and return to you all commissions and income arising. The problem is that because the financial planner has no other sources of income, he will charge you full cost of his professional services which is sometimes can be cost prohibitive for most Malaysians.

3. The advice financial planner gives is holistic in nature

A genuine fee based financial planner helps you to address various issues which include

- income, expenses and debt planning,

- insurance planning,

- tax planning,

- retirement & EPF planning,

- children education funding,

- home purchase and property investment management & planning,

- estate planning and investment planning.

Any financial planner whom you engage with must be competent enough to

- identify your financial goals,

- analyze your current financial standing,

- determine the gap and

- subsequently develop the strategies to achieve your financial goals.

He should have the necessary intellectual framework, advisory model and tools to do the job.

The analogy is similar to a doctor conducting diagnostic tests. He may not prescribe any medicine if not necessary.

Instead, he may just ask you to do more exercise and control your diet. Therefore, you should be on alert if you meet a financial planner who insists on recommending financial products before going through a proper diagnostic process.

What happens when all you are seeking is advice on a specific issue like investment management & planning?

If a one-dimensional financial planner only specializes in this 1 area, he may not be able to foresee how his solutions affect your other financial goals.

When an competent, licensed financial planner can provide multiple advisory services, the result is often very different.

He will be able to align his advice and solutions with your other goals and assets even though he is only engaged to address a specific issue for you.

4. Financial planner has no sales quota to meet

A licensed financial planner has no agency contracts with any financial institutions that manufacture proprietary products like insurance, mutual fund companies or banks.

As such, he will never be under any pressure to sell you these products to meet his sales quotas.

The biggest advantage of this is that you will know that when a licensed financial planner recommends you invest in a product, he is doing it because it fits your financial objectives, not because he has quotas to fulfill.

5. Financial planner has access to a wide range of products

Last but not least, this will give you the opportunity to explore various financial solutions and evaluate the advantages and disadvantages of such options.

Thereafter, he is able to package a combination of financial products to provide the innovative solutions to achieve your financial goals.

Ideally, an independent fee based financial planner has and maintains a strong network of contacts with financial service providers like

- legal firms,

- trustee companies,

- accounting firms,

- tax advisory firms,

- stock broking companies,

- equity fund managers,

- real estate companies and

- banks.

This allow him to refer you the right specialists when required.

With access to financial solutions from multiple providers, a licensed financial planner will also be able to recommend the most competitive solutions.

Ultimately, this benefits you because you have the power to choose and make decisions as an informed consumer.

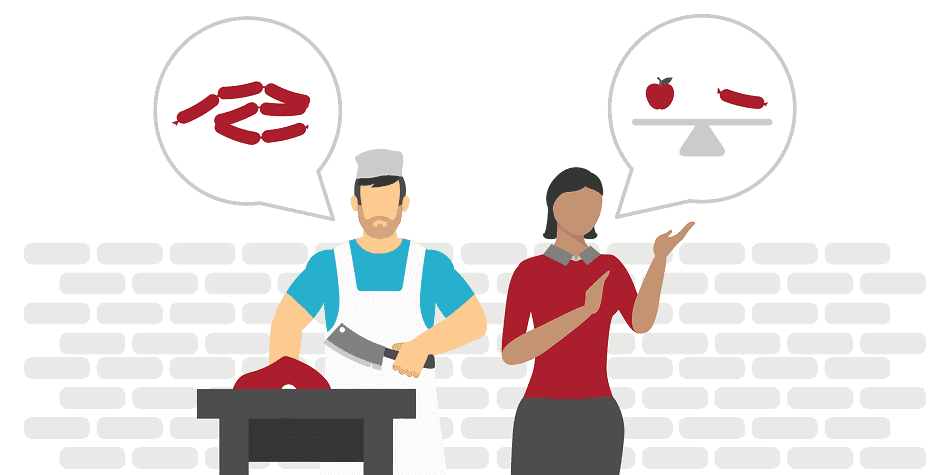

Here’s a quick example to demonstrate.

When you walk into a butcher shop, you are always encouraged to buy meat.

Ask a butcher what’s for dinner, and the answer is always “Meat!”

But a dietitian, on the other hand, will advise you to eat what’s best for your health.

She has no interest in selling you meat if fish is better for you.

Tied financial agents are butchers, while independent consultant are dietitians.

Independent fee based financial planners have no “dog in the race” to sell you a specific product or fund.

In a nutshell, not all certified financial planner professionals are created equal. They are differentiated by ethics and professional responsibilities. The below scale will help you differentiate.

On the left side is a salesman who might be nice and might be sincere.

But, can you be sincere but sincerely wrong, yes or no?

And you move from the left side to the far right, the furthest right is a pure fiduciary, someone who is going to look out for you more than anything else.

But in addition, there are some fiduciaries that would be in the bottom right quadrant. That means they really are fiduciary, but they have low sophistication and low skills. They are very sincere and they’re looking out for your best interest, but they’re not that talented.

You want someone in the upper right quadrant, a trusted independent advisor who will put your interest above anything else, and has the professional responsibility, sophistication and skills to help you turn your financial dreams into a reality.

F) What constitutes a cream of the crop financial planner

How do I choose a financial planner?

What makes you go to one doctor and not another is probably because of things like one doctor having more experience, better communicator with more empathy or having better or more detailed diagnostic process.

The same goes for any financial planner. The 5 MUSTs highlighted just above this section are the pre-conditions that a financial planner must fulfill before you even consult him. Now, we look at some of the criteria which might make you choose one financial planner, but not another.

They say, a picture is worth a thousand words. In the case of any independent financial planner, testimonials from delighted clients are worth more than gold.

Of course, realistically, due to privacy and confidentiality issues, not every clients of a financial planner will be willing to lend his name and face to vouch for the satisfaction & positive income from the advisory work provided.

However, one should expect some sort of testimonials from an experienced financial planner.

“I am an accountant with decent financial knowledge but sessions with CF Lieu provided me with a new perspective and in some cases, details and information that I never knew or considered.

For me the consultancy session provided a lot of value especially with his direct and easy to understand explanations. He is very humble and respectful of client’s viewpoint despite him having a rich knowledge in the financial planning space!”

Sunil Rajamony, GBS Global & Regional APAC Hub Leader and Director Accounting Shared Services APAC, at Huntsman Corporation

A ‘Lecture Session’ Done Well – from a Clinical Professor

Being a clinical professor myself, Lieu’s 1on1 ‘lecture session’ was all well done because it met what I wanted to know. It has helped me to discover a number of things about my insurance policies which I was not even aware of in the first place.

For example, managing insurance coverage sustainability so I know what to expect 20-30 years now, instead of being faced with a rude, shocking discovery of policy lapse or premium spike.

The other important thing is that I am now able ask way better critical questions when any insurance product is recommended to me , instead of just settling for whatever that is being offered.

Personally, I do appreciate and understand that good, no conflict-of-interest advice which comes with a fair professional fee is worth it.

For example, 10x-ing medical coverage with only RM 40 extra per month.

Lieu also gave me investment portfolio management insights that make me rethink how to better my investment strategy going forward.

Dr Teh Wai Choon, Consultant Orthopaedic & Trauma Surgeon at Pantai Hospital, also Clinical Professor at AIMST University

Lieu’s direct advice has helped us pieced together the fragmented parts in our financial situation, confirmed the doubts we have & gave much clarity for us to make informed financial decisions for the better.

KB Ou Yong & KC Neo, Lawyers @ KB Ou Yong & Co

Clarity – Confidence – Conviction – Relatable

The entire course of CF Lieu’s advisory sessions had been a quantum leap for me in having much higher clarity on my financial standings. I can now focus on the matters that truly move the needle and actions which are really aligned to my financial goals.

With clarity, I feel more confident in how much I can spend, how much I can leverage safely still…while still keeping the end goals in mind instead of keep running in circles.

Equipped with higher confidence going forward, I now have more conviction to commit & execute the strategies you recommended. The roadmapping process has revealed to me that I can still have a sustainable retirement portfolio in place 40-years from now without compromising current lifestyle.

I like the fact that CF Lieu is truly relatable as an adviser – you didn’t use any alienating jargons or complex explanations. Yet, you still able to get your point across in a practical & deft manner.

The Exploration and Reflection coaching process was another thing I appreciate much. Never once did I feel cornered throughout our engagement process. In more ways than one, Lieu helped me discovered and surfaced the answers to a web of inter-related questions I had ~ answers which I probably already have within myself but weren’t obvious before.

Azian Ahmad, Head Of Human Resources at Lazada

Biz owner & former regional Head of Human Resource Operations , Shell Business Operations

The advisory sessions are conducted in no rush have been extremely helpful and have clarified a huge amounts of points which I wasn’t aware prior.

I now feel much better equipped to make the right decision being guided step by step by CF Lieu.

Of course the decision will be entirely mine but having the expertise of an expert from Malaysia who clearly understand the law, the rules , the practices if extremely valuable.

Pierre Perusset, General Manager – The Ritz-Carlton Hong Kong

I’ve been engaging CF Lieu for the past couple of months and have so far had 3 sessions with him. I found CF possesses strong financial knowledge to give sound advice. Often people including myself will ask: “Is such financial service worth the money spent? Or are they just too expensive and a waste of money?”

My experience with CF has assured me that it is penny well spent.

Why? The answer is simple.

My realization is that if I pay CF Lieu RM1,000 today, his advice is able to help me invest smarter to gain RM10,000 in the near future. If I pay CF another RM1,000, his advice is able to help me avoid pitfalls that could cause me to lose RM100,000 one day through foolish investment and greed.

Sometimes CF tells me things that I already know. But…there’s a big BUT here…There is a big difference between knowing something and doing something about it. So when advice comes from a credible Financial Planner like CF, it significantly reinforces my earlier beliefs and more importantly, makes me ACT on doing the right thing.

I found CF has been a rather independent financial planner. Impartial in his advice.

Most financial planner’s interest will be to get as much of your life long savings to invest with them. Or to show you maximum returns of your investment so you continue to invest more with them.

So far I appreciate CF’s careful approach and advice. He is able to balance risk vs returns for varying risk profiles of his clients. In this investment game, one can be so blinded with quick high returns, and lose 50% the next day. CF is able to instill the right discipline and advice so that we can still be a prudent and safe long term investor. Thanks for your wisdom and for continuously making a positive difference in people’s financial life!

Khoo Choo Beng, General Manager (Business Excellence) – Sarawak Shell

My dream is to achieve financial independence. I’m sure I’m not the only one.

For years, I’ve been managing my investment portfolio by myself in order to achieve my dreams, and I feel that I’ve finally run into a wall in terms of how much I can optimise my portfolio, due to my own limitations in terms of knowledge and time.

This is when I started to look around for help and stumbled across Lieu’s website. I read the many positive testimonials and watched his YouTube videos, and was convinced enough and decided to reach out to him to seek help on optimizing my investment portfolio.

I was not disappointed. Throughout the fact finding and follow up sessions, I can sense that Lieu was genuine. This was very important to me, as I wasn’t looking for another salesman.

He helped me understand the building blocks of investment, and helped me to understand my current investment portfolio at a deeper level.

He explained things in easy terminologies and used funny analogies, which made things easy to understand.

Afterwards, he would also provide the ‘best and worse case answer sheet’, which provides an alternative solution to my problem.

This was actual actionable and useful advice, and not just another generic advice which we can just get on the internet.

So not only did he teach me how to fish, he also cooked and served me the fish.

And just to make sure I was okay, Lieu even scheduled an additional session with me at no additional cost to ensure I understood everything that he thought me.

In the end, we achieved the objectives that we set out to achieve, and I am happy that I chose Lieu as my financial consultant. I also like to think that I’ve made a new friend along the way.

Thank you Lieu for everything.

Yusma Bazleigh M Yusoff, Senior Geoscientist at PETRONAS

The clarity I got from Lieu’s 1on1 advisory sessions hits me like a boulder! Going forward, I now know how to ask The Right Questions whenever I engage with Financial Intermediaries.

That being said, I truly appreciate Lieu’s very clear & relatable explanation, using analogies that I am familiar with. Especially on understanding the fundamentals of different investment asset classes before jumping into multiple investment platforms – and what to look out for, even when I am short of time, the unskippable MUST-KNOWs.

Big realization – when it comes to insurance & investment, Move Fast & Break things does NOT work; it is indeed very costly to fix or reverse a non-ideal financial decision.

But like they said – better late than never!

Vivien L, Senior Marketing Manager, Intelligent Money S/B

Tan Sun Yau, CFO, IBM Malaysia (1978-2007)

Testimonials from Dr Thinakaran Malapan, 40 (Ipoh), married with 2 children, Gynecologist with Tropicana Medical Center

CF Lieu helped me to conduct a thorough tax planning for my private practice and investment portfolio.

He came to me at the right timing of my career and, in turn I engaged him for fees-based advisory.

I never would have thought a financial planner can do advanced company & property tax planning, so I really credit CF for a a fee-based advisory nicely done – giving me and my wife much clarity on the overall big picture.

The approach

CF gave me ample of time to clear my doubts, me being not coming from financial background, albeit being an analytical person. The process is like this – After coming out with the first drafts of the tax planning advisory reports, which CF will send to me to digest, then we will have discussions to clarify/fine-tune/amend the sections where required.

The response time is good; CF is contactable and the follow-ups meet my expectation.

The ROI

The advisory fees are not cheap – that’s what I feel when we started. However, I’d say it is certainly affordable.

Only after I experienced the approach CF delivered the end result, I can vouch it is certainly worth the professional fees.

Evidently, there are aspects in my investment properties portfolio which needs to be fined-tuned. Without going into details, these “fine-tunes” saves me money in the long run which is way more than the fees charged. Also, cost savings tips and tricks I’d would not have known if I didn’t go thru the advisory process.

I can vouch for CF in delivering quality advisory work to clients.

**********

Testimonials from Dr Hans Lim, 34 (Penang), married with 2 children, General Practitioner

Quotes from Dr Hans Lim

I liked your approach of advising without financial jargons, just plain english, something I can relate.

Fees are affordable, and most importantly, from neutral perspective.

From medical perspective, you are prescribing medicine that you are actually eating

**********

Personally, even financial institutions like Maybank and investment management companies like Permodalan Nasional Bhd engaged me to train their staff.

More clients testimonials here

G) 11 types of financial advice should you expect from a financial planner

- Be in writing

- Be without obligation

- Focus on your financial goals

- Be Impartial

- Take into account your cash flow requirements and need for spare cash

- Disclose any entry fees, exit fees and any other costs to you in the future

- Justify the reasons for selecting the proposed investments or recommendations

- Divulge all inherent risks associated with the recommendations

- Spread your investments across different assets

- Highlight any tax implications

- Give options on how to pay for your investments

H) 6 Things NOT to expect from your financial planner

Any productive and meaningful relationship between you and your financial planner rests on both parties playing their roles in managing your personal finances.

With that in mind, there are 2 things required of you to ensure that there is little deviation from your path towards attaining financial freedom.

Commitment and Time

You must commit and don’t be half hearted half way through the process. Even the most competent & dedicated financial planner in cannot achieve much for you if you are not accountable for your own financial goals.

Although you can now delegate many of the tasks in managing your personal finances to a trusted financial planner, it does not mean you can forget about it altogether.

You still have to make time to meet him on regular basis to enable him to give you progress report as where you stand financially.

The financial planner need to get your consent to execute necessary actions. Ideally, set aside about 2 hours each month to meet with your financial planner during the first year, and probably about 5 times a year in the following years.

Now, come to what you can realistically expect from an independent financial planner. If your expectations are unrealistic, you might find reasons to terminate your professional relationship and that could lead you to changing financial planners regularly.

Unfortunately, this will adversely affect your financial standings, disrupt your personal financial management, affect your investment performance and increase your expenses.

As a result, you will be running out of time to achieve financial freedom. Here are the few things you should not expect from an independent financial planner:

1. Don’t say to your independent financial planner: “You must guarantee my investments will make money even if the economy is bad”

Investment management wise, a financial planner would not be able to make your investments grow when market is in a downtrend unless he is also running a hedge fund or private equity fund (unlikely).

However, if he has done a good job of proper asset allocation and informed diversification, ‘best of breed’ fund selection and rebalancing, your investment won’t suffer as much in bear market

2. Don’t say to your independent financial planner: “You must guarantee that my investments will outperform the market when the market is up”

Again, if your independent financial planner does proper asset allocation and diversification into multiple asset classes, this is unlikely to occur. For example, when market is up by 30% in a particular year, but bond market only up by 5%, you may expect your investment return goes up to 40%.

A proper asset allocation might put your portfolio weightage as 40% bonds, so your portfolio can actually be up, say, 20% only.

On the other hand, your portfolio would have beaten the stock market when equity market is going down as bond outperform stocks.

Remember, your independent financial planner main job is not beating the market, but to optimize your long term investment returns by reducing their volatility.

Most importantly, a real financial planner should be the thing between YOU and the BIG MISTAKE – in other words, someone who helps you to manage things which you can control (risks) instead of promising you high returns (which no one can control).

3. Don’t expect your independent financial planner to agree with everything you say; keep an open mind to his recommendations

An independent planner has the duty to help you manage your finances effectively. It is normal if his advice or recommendations contradicts with yours at times.

For example, you may be an avid property investor and may have made substantial money from your historical purchase. Confident, you put 90% of your investable assets in properties. From prudent financial planning perspective, such concentrated portfolio has its inherent risks.

Do not be upset when your independent planner suggests you divest some of your holdings into more liquid portfolios.

Don’t close your mind and start judging him and questioning his agenda. Instead, listen to what he has to say, give feedback and voice your concerns in a two way discussion.

Never shut down any communication between you and your independent financial planner without giving him any chance to justify his recommendations.

4. Do not expect your independent financial planner to produce immediate results

Your independent financial planner who is also your investment portfolio manager, similar to wealth manager at banking institutions, will need time to deliver investment performance.

A reasonable period to allow your financial planner to deliver results is at least 5 years or a full market cycle.

For example, do not terminate his services if you experience negative returns after 1 year investing which coincide with bear market or market correction. Your independent financial planner deserves more time to prove the success of the holistic plan he has developed for you.

6. You must share information and any concerns you have with your independent financial planner

As the saying goes, garbage in, garbage out. If you do not provide accurate and timely information to your independent financial planner, he will not be able to provide effective services.

Furthermore, by being open in what concerns you, your independent financial planner will be in a position to suggest customized strategies to help you.

Beware that you can only expect lower quality advice and service from your independent financial planner if you have withheld information from him.

I) Should you Start Now?

Failing to plan is actually planning to fail because procrastination is the world’s greatest wealth killer.

Every day you wait to get started makes your financial goals more difficult to achieve because it burns your greatest asset – time – the one thing that is irreplaceable.

If you want to provide more for your family and security for yourself then you are in the right place.

Fee based, independent financial advisory is about a step-by-step roadmap to financial freedom so you can successfully clear the hurdles and avoid the potholes that inevitably pop up along the way. It is a single, comprehensive, soup-to-nuts, structured learning process showing you the way to succeed with more security and confidence.

Let’s face it. You don’t need another seminar. And you don’t need more books or articles.

What you need is results. You need a structured environment with the accountability adviser, and information to pull you toward your goals with the least effort and resistance possible.

If you are tired of sitting on the sidelines and under-performing your potential then this could bring you to a new level.

If you are tired of all the contradictory information and biased half-truths then you are in the right place.

Conclusion

As the public get savvier and financial markets mature, independence in fee-based financial planning will get increasingly popular.

This is when the trend turns away from ubiquitous financial products and homogeneous asset management or unit trust companies.

The general public who appreciate the nuances between different financial products and understand that there are more than just the good “highlights” of what tied agents tell you will start to appreciate independent financial planner.

Independent financial planner does not enjoy the privilege of being backed by an insurance company or associated with unit trust companies. It is relatively small, compared to the existing agencies structure everywhere.

But being small and independent offers some specific advantages. For example, tied agents trained by agencies can be strongly encouraged to recommend the more profitable products, which may not be in the client’s best interest.

But independence is still under appreciated as the possible conflict of interests that can arise from being tied to another institution with its own set of priorities are rarely highlighted.

That’s why no agencies can do away with the quota system, while independent advisory can. It takes time for independent financial planner to explain the value and importance of independence to our potential clients.

Independence is not something highlighted in our market and most people are not used to financial services that are not owned or backed by a brand name we are familiar with.

Now It’s Your Turn

Phew! We put A TON of work into this guide. So we hope you enjoyed it.

Now we’d like to hear what you have to say.

Did we answer all your questions or doubts above? Or something still missing?

Let me know by leaving a comment below.

4 Places to Find A Financial Planner in Malaysia

MY EXPERIENCE WITH A LICENSED FINANCIAL PLANNER IN MALAYSIA

My 2-year experience with a Licensed Financial Planner in Malaysia

Thanks for the value packed info!

These 52 tips for hiring an authentic financial planner are perfect for me, and I am incredibly thankful that these tips have been shared here. I hope that the financial planner I hire will do a fantastic job.

Need to consult on consolidation

Lynn, Consolidation on? 🙂